Pursuant to our yearly audit of state-specific disclosures, we will be creating three new documents for loans secured by property in Washington, as well as modifying two Washington-specific disclosures:

New Documents:

WA Mortgage Insurance Cancellation Disclosure and WA RD Mortgage Insurance Cancellation Disclosure (Cx18541 & 18542)

These documents are being created pursuant to Wash. Rev. Code Ann. § 61.10.020(1), which requires the following:

“If a borrower is required to obtain and maintain mortgage insurance as a condition of entering into a residential mortgage transaction, the lender shall disclose to the borrower whether and under what conditions the borrower has the right to cancel the mortgage insurance in the future.”

While the disclosures required under the Federal Homeowner’s Protection Act (Cx29, Cx862, Cx4668, Cx16990, Cx16991, and Cx16992) are adequate for complying with this section of law in regards to loans secured by single-family dwellings (which the HPA only applies to; see 12 USCA § 4901[15] & [17] and 4903), Washington’s provisions apply to loans secured by one-to-four unit properties (see Supra § 61.10.010[3]).

Thus, there is some overlap between these two laws: Federal law governs the disclosures for loans secured by single family units (see Ibid. § 4908 and Supra § 61.10.040), while Washington law governs the same disclosures for loans secured by two-to-four unit properties.

In addition, while Washington’s laws concerning the cancellation of PMI set forth the conditions under which it may be cancelled (see Supra § 61.10.030[1]), an exemption is carved out for loans which will be sold to an “institutional third party,” such as the Federal National Mortgage Association (FNMA) and Federal Home Loan Mortgage Corporation (FHLMC). In such cases, the rules concerning cancellation by these institutions may be adhered to.

Exemptions to the disclosure rules are also carved out for loans which are serviced in accordance with federal requirements (i.e. FHA and VA loans)

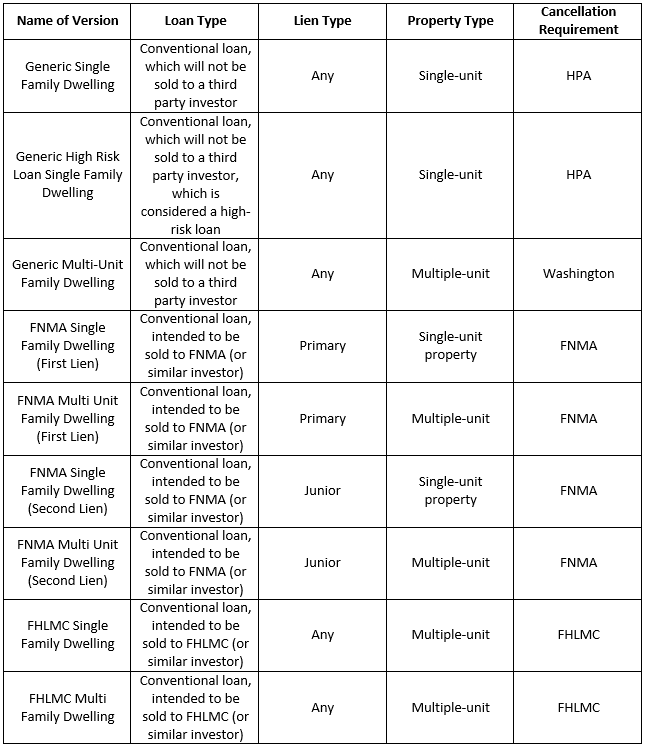

This means that, in regards to two-to-four unit dwellings, a disclosure separate from the Federal ones must be provided, but they must vary in disclosing the terms of cancellation based upon whether they are being sold to FNMA or FHLMC, or whether it is not being sold to either of these investors (or ones with substantially similar requirements).

Due to this, we will be providing Cx18541, which will contain dynamic text which will print the cancellation guidelines set forth by Federal or Washington law, or FNMA or FHLMC guidelines. Thus, nine versions of this document will print based on who the investor is, what type of lien position the loan will be in, and the property it will be secured by:

This document will print under the following conditions:

- “Base Type” equals “Conventional”;

- “Document Package Type” equals “Initial Disclosure”;

- “Monthly Mortgage Insurance” equals “Yes”;

- “Occupancy” equals “PrimaryResidence”; and

- “State Code” equals “Washington”.

Although FHA-insured and VA-guaranteed loans are exempt, there are no exemptions for RD loan programs and the annual guarantee fee which is imposed by them, which fee can be considered the equivalent of a mortgage insurance premium. Due to this, we will be providing a separate document (Cx18542) for RD loans, which simply informs the borrower that they do not have the right to cancel the guarantee during the life of the loan.

WA Commitment Agreement (Cx18562)

Wash. Rev. Code Ann. § 48.30.260(3) imposes the following restriction:

“No person who lends money or extends credit may:

(a) Solicit insurance for the protection of property, after a person indicates interest in securing a loan or credit extension, until such person has received a commitment from the lender as to a loan or credit extension.”

In order to help clients not to violate this restriction, we will be providing Cx18562, which will print under the following conditions:

- “Disclosure Package Type” equals “Initial Disclosures”;

- “Mortgage Loan Commitment” equals “Yes”; and

- “State Code” equals “Washington”.

Changes to Current Documents

We will be modifying WA Disclosure Receipt (Cx3747), provided due to the provisions of Wash. Admin. Code § 208-620-510(2), in the following ways:

- The text preceding the list of documents will be combined into one sentence, which will be left-align (rather than center-aligned, as they are now);

- Rather than printing the hard-coded text for the list of disclosures, we will be using Field dt_HTMLDocList2/@v, which should generate a list of the disclosures that the borrower received in their Initial Disclosure package;

- If either of the following conditions are met, the list will include a reference to the Settlement Cost Booklet:

- When both:

- “Loan Purpose” equals either “Purchase”, “Construction”, or “ConstPerm”; and

- “Lien Position” equals “FirstLien”; or

- When “HUD Booklet Inclusion” equals “InAllPackages”; and

- When both:

- If any of the following conditions are met, the list will include a reference to the CHARM Booklet:

- When “CHARM Booklet Inclusion” equals “InAllPackages”;

- When both:

- “CHARM Booklet Inclusion” equals “AllARMLoans”;

- “Amortization Type” equals either “AdjustableRate” or “Neg-Am”; or

- When:

- “CHARM Booklet Inclusion” equals “ARMLoansExceptHELOCS”;

- “Amortization Type” equals either “AdjustableRate” or “Neg-Am”; and

- “HELOC” equals “No”.

We will also be including the following text to the first paragraph of the Washington-specific version of the Tangible Net Benefit Worksheet (Cx12531):

“For a list of fees being charged in connection with this transaction, please see the accompanying Itemization of Amount Financed.”

This is being added due to the following provisions of Wash. Admin. Code § 208-620-560(4)(d):

“The limits in (a) and (b) of this subsection do not apply if you can demonstrate a net tangible benefit to the borrower for the new loan or credit line increase. For purposes of this subsection a net tangible benefit may be demonstrated by a lower monthly payment, or a decrease in the interest rate. Any net tangible benefit analysis must include the fees or charges for the new loan or credit line increase.” (emphasis added)

These changes will take effect on August 15, 2014. If you have any questions or concerns about these changes, please contact Client Support at 1.800.497.3584.

August 8, 2014

DR 150126 and DR 150104

Update:

Upon further review, we will be configuring the new Washington PMI Disclosures (Cx18541 and 18542) to print in Closing packages, per the requirements of Wash. Rev. Code Ann. § 61.10.020(1)(c) that the disclosures be provided ‘at the time the transaction is entered into,’ rather than in Initial Disclosure packages.

August 13, 2014